A common measure of operating profitability is ROIC, the Return on Invested Capital. The idea is (appropriately) to measure profitability that is independent of how the business operation is financed. Calculated correctly, ROIC is the same as RNOA, but it often is not. A common calculation is

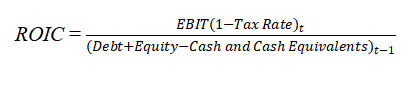

This adjusts EBIT for taxes, but at the statutory tax rate rather than the effective rate. And the denominator, while taking out cash and equivalents, leaves in other debt assets in short-term investments. More significantly, it does not incorporate operating liabilities.

In calculating their moat index, S&P Global calculate ROIC as

Total Debt is not net debt. It should be reduced by debt assets, and it should be by reduced operating liabilities. That then yields net financing debt which, added to total shareholders’ equity yields net operating assets. Net Income in the numerator includes net interest on debt and taxes on net interest. This is part of financing, not operations. Not good.