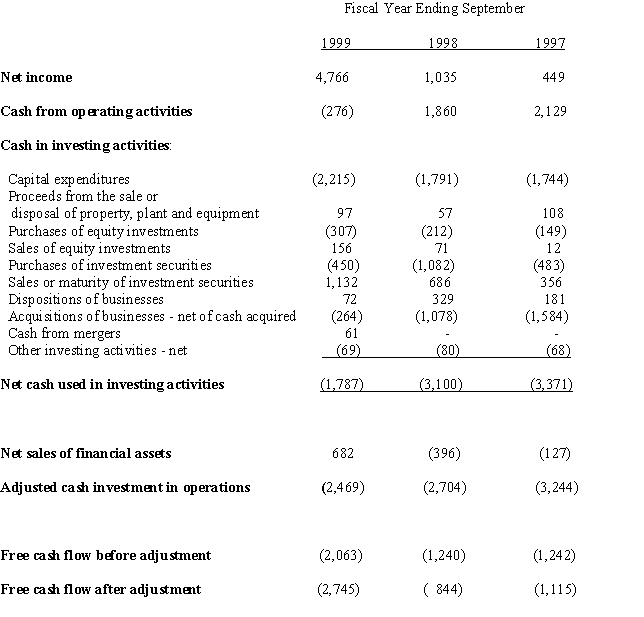

GAAP and IFRS err on treating purchases and sales of debt investment as investment in operations. That can lead to grave errors in understanding the cash flows of a business. Here is an example for Lucent Technologies (in $millions):

You can see that the firm, while generating positive net income, generated negative cash flow from operations in 1999. Its operations are absorbing cash, not generating cash; it has potential liquidity problem. At the same time, it is liquidating a net $682 million in debt assets by $682 million to meet the shortfall. But this is treated as a reduction in cash investment in operations. That makes free cash flow lower than it should be, so seemingly operations are using less cash. In 1998 and 1997, it goes the other way.

In 2023, Meta Platforms (Facebook) spent $27.7 billion investing in its business but sold off debt assets for a net $3.2 billion to make the investments. The latter was included in cash investment to report a total of $24.5 billion rather than the $27.7 billion.

In its December 2024 quarter, Apple Inc. reported a positive number, $1,927 million for cash investment in operations, looking as if investing activities were generating cash rather than using it. However, the cash investment section of the cash flow statement included a net $4,603 million from liquidating debt assets. The actual cash expenditure in operations was $2,676 million. As these and other firms invest heavily AI, watch the cash investment number: They might be liquidating their big debt asset holdings to do so.